Introduction

Access to credit is a cornerstone of rural economic development. In many regions, financial inclusion is crucial for empowering individuals and communities in rural areas. This introduction explores the various sources of rural credit, encompassing traditional financial institutions, government initiatives, and innovative models. Understanding these sources is essential for fostering financial stability, promoting entrepreneurship, and addressing the unique needs of rural populations. Whether through conventional banking or targeted schemes, the availability of rural credit plays a pivotal role in driving sustainable growth and improving the quality of life in rural communities.

What Are the Informal Sources of Rural Credit in India?

In India, informal sources of rural credit play a significant role in meeting the financial needs of rural communities where formal banking infrastructure may be limited. These informal sources include.

| Moneylenders | MicroFinance Institutions | Self-Help Groups |

| Traders & Merchants | Cooperatives | Pawnbrokers |

| Landlords | Agricultural Input Dealers | Friends & Relatives |

Moneylenders- Independent individuals who lend money to farmers and rural households. Moneylenders often operate independently and charge higher interest rates compared to formal financial institutions.

Traders and Merchants- Local traders and merchants in rural areas extend credit to farmers for the purchase of agricultural inputs or to facilitate trade. Credit terms are often tied to the sale of the farmers’ produce.

Landlords- In certain situations, landlords may provide credit to tenant farmers or sharecroppers based on informal agreements related to land cultivation. This practice is deeply rooted in traditional agrarian relationships.

Friends and Relatives- Borrowing from friends and relatives is a prevalent practice in rural India. These informal arrangements rely on personal relationships and trust, with terms often based on mutual understanding.

Self-Help Groups (SHGs)- Community-based organizations where members contribute to a common fund. Loans are then provided to group members based on their needs, fostering financial inclusion and community support.

Microfinance Institutions- Non-banking financial institutions that operate in rural areas, provide small loans to individuals—particularly women—for income-generating activities. This supports entrepreneurship and financial empowerment.

Cooperatives- While some cooperatives are formal entities, others operate less formally in rural areas, providing credit to their members for agricultural and community development.

Agricultural Input Dealers- Sellers of agricultural inputs, such as seeds and fertilizers, may offer credit facilities to farmers, allowing them to purchase inputs on credit and repay after the harvest.

Pawnbrokers- Farmers may approach pawnbrokers and use assets like jewelry or equipment as collateral to secure loans. However, this source often involves high-interest rates.

These informal sources of rural credit are deeply embedded in the socio-economic fabric of rural India. It is, therefore, imperative that several challenges, such as extremely high interest rates, lack of formal documentation, and limited regulatory oversight be removed despite being a lifeline to financial support in creating a fair lending environment. An attempt is being made to maintain a balance of these sources between the preservation of flexibility and protection of the interests in respect of the rural borrowers.

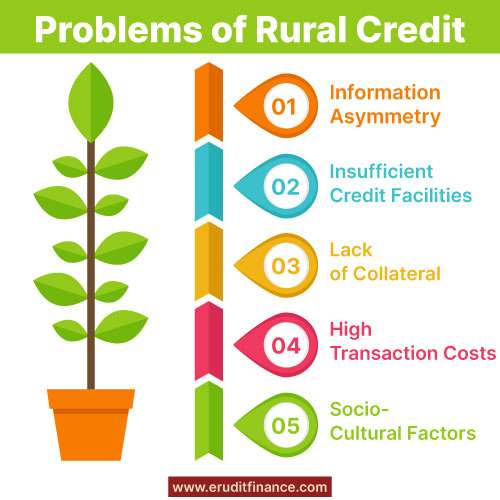

What Are the Problems of Rural Credit in India?

Rural credit in India faces several challenges, impacting the accessibility and effectiveness of financial services in rural areas. Some prominent problems include.

Lack of Formal Banking Infrastructure- Many rural areas lack adequate formal banking infrastructure, making it challenging for farmers to access financial services. Limited bank branches and ATMs in remote regions hinder financial inclusion.

Dependence on Non-Institutional Sources- A significant portion of rural credit comes from non-institutional sources like moneylenders, who often charge exorbitant interest rates. Dependence on such sources can lead to debt traps for farmers.

Insufficient Credit Facilities- Small and marginal farmers often face difficulties in obtaining sufficient credit to meet their agricultural and livelihood needs. Inadequate credit limits can constrain agricultural productivity.

Seasonal Nature of Agriculture- Agriculture is inherently seasonal, with income generated mainly during harvest periods. Farmers may face challenges in repaying loans during non-harvest seasons, leading to financial stress.

Lack of Collateral- Traditional lending practices often require collateral, which many smallholder farmers may not possess. The absence of viable collateral options limits their access to formal credit.

Information Asymmetry- Lack of awareness about various financial products and services, coupled with low financial literacy, contributes to information asymmetry. Farmers may not fully understand the terms and conditions of loans.

Inadequate Risk Mitigation- Agriculture is susceptible to various risks such as weather fluctuations, pests, and market uncertainties. The absence of effective risk mitigation measures, including crop insurance, leaves farmers vulnerable.

High Transaction Costs- The high transaction costs associated with obtaining and servicing loans, particularly for small amounts, can make formal credit less attractive to both lenders and borrowers.

Limited Digital Financial Inclusion- While digital finance has the potential to enhance financial inclusion, rural areas often face challenges related to internet connectivity, digital literacy, and the availability of digital financial services.

Policy and Implementation Gaps- Policy and implementation gaps at the grassroots level can hinder the effective execution of rural credit schemes. Delays in disbursing loans and inadequacies in reaching the intended beneficiaries are common issues.

Socio-Cultural Factors- Socio-cultural factors, including caste dynamics and traditional norms, can influence access to credit. Certain social groups may face discrimination or exclusion from formal financial channels.

Addressing these challenges requires a holistic approach involving the expansion of formal banking infrastructure, targeted financial literacy programs, innovative risk mitigation mechanisms, and policy interventions to enhance the inclusivity and effectiveness of rural credit in India.

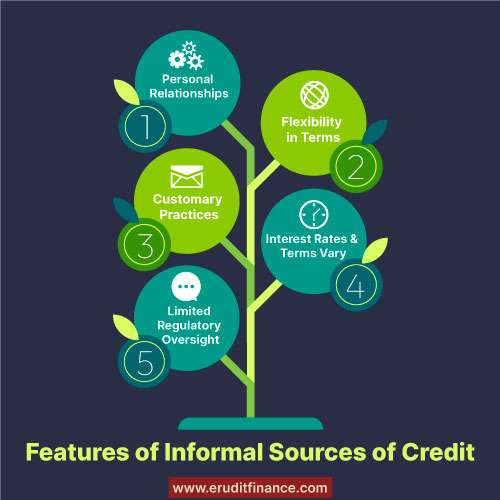

What Are the Features of Informal Sources of Credit?

Informal sources of credit, characterized by their flexibility and community-oriented nature, exhibit several distinctive features. These features highlight the informal nature and dynamics of these credit sources.

a). Personal Relationships: Informal credit often relies on personal relationships and trust. Borrowers may have pre-existing connections with lenders, such as being friends, relatives, or members of the same community.

b). Lack of Formal Documentation: Transactions in informal credit typically lack formal documentation. Unlike formal institutions that require extensive paperwork, informal sources may operate based on verbal agreements or simple written records.

c). Flexibility in Terms: Informal credit arrangements often allow for flexible and negotiable terms. Interest rates, repayment schedules, and other conditions may be adjusted based on the borrower’s circumstances and the lender’s understanding.

d). Quick Decision-Making: Informal sources can provide quicker decision-making processes compared to formal institutions. The absence of bureaucratic procedures allows for swift responses to the financial needs of borrowers.

e). Localized and Community-Based: Informal credit is deeply rooted in local communities. Lenders may be part of the same community or have a direct understanding of the local socio-economic dynamics, making credit more attuned to the borrowers’ needs.

f). Limited Regulatory Oversight: Unlike formal financial institutions that are subject to regulatory scrutiny, informal sources operate with minimal regulatory oversight. This lack of formal regulation can lead to both advantages and challenges for borrowers.

g). Interest Rates and Terms Vary: Interest rates in informal credit arrangements can vary widely and may be influenced by factors such as the relationship between the lender and borrower, the urgency of the need, and prevailing socio-economic conditions.

h). Collateral May Not Be Required: Informal credit may not always necessitate collateral. Borrowers may secure loans based on personal trust, reputation, or verbal agreements rather than tangible assets.

i). Socio-Cultural Influences: Socio-cultural factors, including caste, kinship, and community ties, may play a role in informal credit. These factors can influence lending decisions and relationships within the community.

j). Customary Practices: Informal credit often adheres to customary practices prevalent in the community. This could include following traditional norms and practices related to lending and borrowing.

k). Accessibility in Remote Areas: Informal sources of credit may be more accessible in remote or underserved areas where formal financial institutions have limited reach. Local individuals or groups may fill the void in financial services.

While informal sources of credit contribute to financial inclusion and community cohesion, they also pose challenges such as lack of consumer protection, potential exploitation, and limited avenues for dispute resolution. Balancing the advantages and risks requires efforts to enhance financial literacy, regulate certain aspects, and integrate these sources into broader financial inclusion strategies.

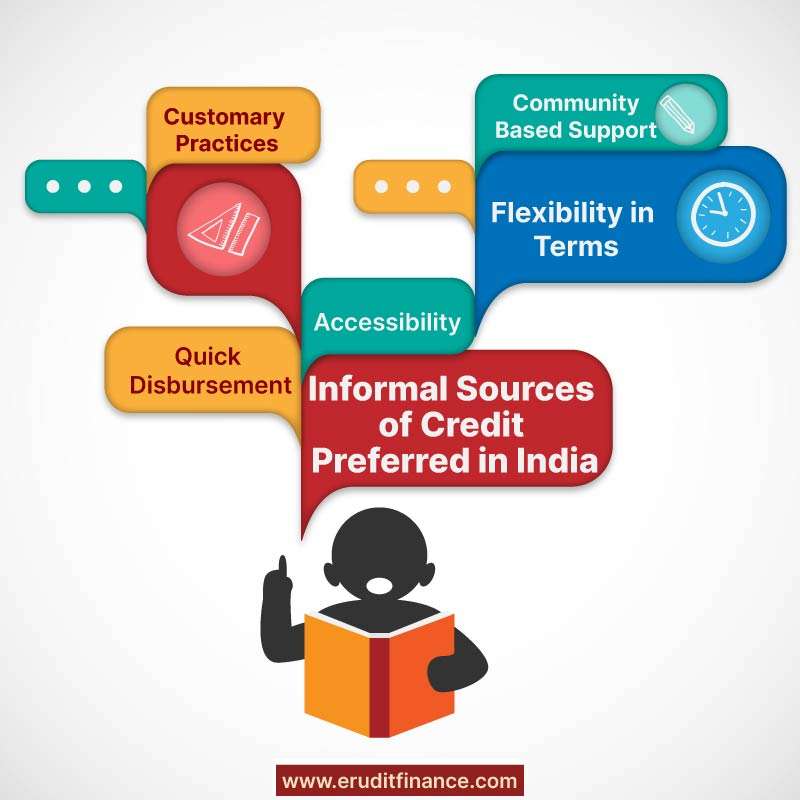

Why Are Informal Sources of Credit Preferred in India?

Informal sources of credit are often preferred in India for several reasons, reflecting the unique socio-economic landscape and challenges faced by individuals, especially in rural areas. Here are some key reasons why informal sources of credit are commonly chosen.

Accessibility- Informal sources are often more accessible, especially in remote or underserved areas where formal banking infrastructure may be limited. Local moneylenders and community members are readily available to provide credit.

Quick Disbursement- Informal sources can disburse funds quickly. The absence of complex paperwork and bureaucratic processes allows for swift decision-making and immediate access to funds, which is crucial, particularly in emergencies.

Personal Relationships and Trust- Borrowers often have pre-existing personal relationships with informal lenders, such as friends, relatives, or members of the same community. Trust plays a significant role, making the borrowing process more comfortable and informal.

Lack of Formal Documentation- Formal financial institutions often require extensive documentation, which can be a barrier for individuals with limited literacy or those residing in remote areas. Informal sources operate with minimal or no formal documentation, reducing the bureaucratic burden.

Flexibility in Terms- Informal credit arrangements offer flexibility in terms of interest rates, repayment schedules, and loan amounts. Lenders may tailor terms based on the borrower’s specific needs and circumstances.

Customary Practices- Informal credit often aligns with customary practices prevalent in the community. Borrowers and lenders may follow traditional norms and practices, making the credit process more familiar and culturally embedded.

Lack of Collateral Requirement- Informal sources may not always demand collateral. This is particularly beneficial for borrowers who may not possess tangible assets, providing them with access to credit based on personal relationships or verbal agreements.

Community-Based Support- Informal sources are embedded in the local community, and lending decisions may consider broader community dynamics. This community-based support can foster a sense of solidarity and mutual assistance.

Limited Alternative Options- In regions with limited formal financial institutions, individuals may resort to informal sources due to the absence of alternative options. The convenience and accessibility of informal credit become essential in such contexts.

Informal Economy Dominance- A significant portion of economic operations in India are in the informal sector. People engaged in informal businesses or occupations may find it more practical to seek credit from sources within the informal economy.

While informal sources of credit address immediate financial needs, it’s crucial to acknowledge the challenges associated with them, such as high-interest rates, lack of consumer protection, and potential exploitation. Efforts are underway to strike a balance between leveraging the advantages of informal credit and integrating it into broader financial inclusion strategies with enhanced regulatory oversight.

Bottomline:-

In rural settings, the diverse sources of credit, ranging from formal banking institutions to informal community-based arrangements, form a crucial financial ecosystem. While formal sources provide structured financial products, informal channels offer accessibility and flexibility. The interplay between these sources reflects the complexity of rural credit dynamics, shaped by local needs, personal relationships, and traditional practices. Striking a balance between the advantages of accessibility and the challenges of informal credit requires targeted interventions, financial literacy initiatives, and regulatory measures to ensure fair and responsible lending practices in rural areas.

Also Read:

Whats up very nice site!! Man .. Beautiful .. Amazing .. I’ll bookmark your blog and take the feeds also…I’m happy to find numerous helpful info here in the submit, we want develop more techniques on this regard, thank you for sharing. . . . . .